Throughout the peak days of the COVID-19 pandemic, individuals world wide more and more adopted a work-from-home atmosphere and started discovering new methods to entertain themselves when obligation didn’t name.

A kind of areas was the inventory market. Shares in all industrial sectors fluctuated for causes fully unrelated to actuality. In some ways, the inventory market has change into a digital on line casino, and plenty of unsuspecting traders discovered a harsh lesson: Shares don't go up ceaselessly.

One inventory that noticed unmatched highs through the peak of the pandemic was the web vogue retailer. sew association (NASDAQ:SFIX). What was as soon as a inventory buying and selling at $106 per share is now simply $2.74, down 97% from its highs.

Beneath, I discover the rise and fall of Sew Repair and clarify why I believe the corporate is a robust candidate for the proper companion to accumulate.

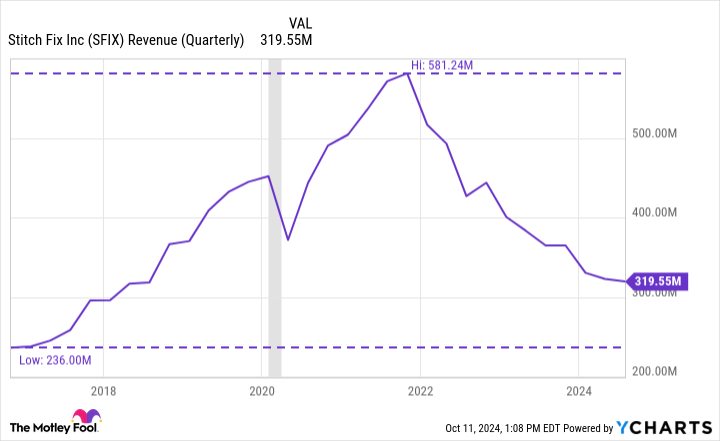

This chart explains all of it.

The chart beneath illustrates Sew Repair's quarterly income since going public. Throughout its first few years as a public firm, Sew Repair constantly generated respectable ranges of development. In 2020, these tendencies took an entire new flip.

The grey shaded column of the graph represents the temporary COVID-19 recession. Whereas income initially fell in early 2020, Sew Repair rebounded spectacularly and witnessed file development that lasted till the top of 2022.

What occurred and why does Sew Repair hold crashing?

The straightforward clarification is that Sew Repair supplied a degree of comfort that was arduous to match through the peak days of COVID-19. Whereas workplace buildings remained closed and brick-and-mortar shops noticed decreased foot visitors, demand for on-line platforms like Sew Repair took off.

In different phrases, Sew Repair was nicely positioned throughout an in any other case once-in-a-lifetime occasion. As soon as the “new regular” slowly got here into impact, individuals regularly reintegrated into society, reviving previous buying habits and preferences.

Along with a broader social reopening, the macroeconomy has been scuffling with persistent inflation for a few years. When the prices of products and providers improve, customers' buying energy weakens. In flip, individuals have to make selections about how and the place they spend cash.

Discretionary companies like Sew Repair are extra of a luxurious and never essentially a necessity. The next desk illustrates the turnover of the corporate's lively prospects over the previous few years.

|

Class |

August 1, 2020 |

July 31, 2021 |

July 30, 2022 |

July 29, 2023 |

August three, 2024 |

|---|---|---|---|---|---|

|

Energetic purchasers |

three.5 million |

four.2 million |

three.eight million |

three.1 million |

2.5 million |

Knowledge supply: Sew Repair.

Clearly, Sew Repair has struggled to retain prospects, which is undermining the corporate's development potential.

Why I Suppose Sew Repair Will Be Acquired

A shrinking buyer base and declining income tendencies go hand in hand. The place I believe Sew Repair actually went off target is the place administration determined to allocate capital.

The corporate tried to distinguish itself from different on-line outfitters by investing closely in synthetic intelligence (AI) and information science. The thought was for Sew Repair to gather information on what clothes gadgets its prospects bought and returned to get a greater concept of customers' buying patterns and preferences. In flip, by understanding the shopper on a deeper degree, Sew Repair may, in concept, leverage its database to drive larger engagement from its customers.

This concept is sort of widespread on e-commerce platforms. This brings me to my record of potential consumers:

1. Amazon: One of the revolutionary concepts within the historical past of this firm is its Prime subscription service. Prime members obtain a mess of advantages, together with free delivery, entry to quite a lot of streaming platforms, and early entry to new merchandise. I consider Amazon has the power to make use of Sew Repair buyer information in its on-line market and the service could possibly be a further profit for Prime subscribers.

2. city suppliers: I see City Outfitters as one other logical candidate to accumulate Sew Repair. The corporate owns a number of shops, together with Anthropologie, Free Folks, and, after all, City Outfitters. These shops supply a big selection of clothes that appeals to varied demographic teams, particularly the extremely contested Era Z and millennials.

Moreover, City Outfitters already has a subscription-based on-line clothes rental asset, referred to as Nuuly. Whereas it's nonetheless early days for Nuuly, traction for the phase has been fairly good to date. I believe Sew Repair may function a complement to Nuuly and develop City Outfitters' on-line presence.

The ultimate end result

I believe it will likely be tough for Sew Repair to get well. The corporate appears misplaced and I doubt administration can proper the ship by itself.

That being mentioned, there are some positives that shouldn’t be discounted. The corporate nonetheless serves tens of millions of individuals and collects invaluable information from its consumers. I believe a bigger firm like Amazon may higher leverage this information and combine the Sew Repair platform seamlessly into their ecosystem. City Outfitters additionally seems to be like a pretty potential companion, given its success with youthful demographics and on-line clothes subscriptions.

To me, Sew Repair is nonetheless a invaluable asset, but it surely's time for the corporate to think about promoting it and partnering with a bigger firm.

Don't Miss This Second Likelihood at a Doubtlessly Profitable Alternative

Have you ever ever felt such as you missed the boat when shopping for the most well liked shares? Then you definately'll need to hear this.

On uncommon events, our skilled staff of analysts points a “Double wager” actions suggestion for firms that consider they’re about to blow up. Should you're fearful you've missed a possibility to speculate, now could be the most effective time to purchase earlier than it's too late. And the numbers communicate for themselves:

-

Amazon: Should you invested $1,000 after we doubled down in 2010, you’ll have $21,266!*

-

Apple: Should you invested $1,000 after we doubled down in 2008, you’ll have $43,047!*

-

netflix: Should you invested $1,000 after we doubled down in 2004, you’ll have $389,794!*

Proper now, we’re issuing “double wager” alerts for 3 unimaginable firms and there might not be one other alternative like this anytime quickly.

See three “double wager” actions »

*Inventory Advisor returns from October 14, 2024

John Mackey, former CEO of Complete Meals Market, an Amazon subsidiary, is a member of The Motley Idiot's board of administrators. Adam Spatacco has positions at Amazon. The Motley Idiot has scores and recommends Amazon. The Motley Idiot recommends Sew Repair. The Motley Idiot has a disclosure coverage.

Prediction: These vogue retail shares are down 97% from their highs and could possibly be purchased over the subsequent 12 months. Right here's why. was initially revealed by The Motley Idiot