Because the Industrial Revolution of the late 1700s, know-how has knowledgeable and pushed numerous radical adjustments in our societies and economies. The tempo has accelerated in latest a long time because the world has gone digital, and now AI is fueling a so-called fourth industrial revolution based mostly on the fast change of information and data.

Towards this backdrop, know-how shares led the best way out there's positive factors. The NASDAQ is up 43% final yr and the S&P 500 is up 24%. Each indexes proceed to publish sturdy numbers this yr; for the yr 2024 so far, they’ve elevated by 24% and 17%, respectively.

This has made Wedbush know-how analyst and professional Daniel Ives bullish on tech shares, noting, “The primary half of 2024 has been a really sturdy run for tech shares, led by Massive Tech cats Nvidia, Microsoft , Amazon, Meta, as a result of this fourth industrial revolution simply occurred. In our opinion, it began to play out at this level in 1995 (not 1999), with many bears nonetheless screaming from their hibernation caves… We expect the NASDAQ nonetheless has a powerful 2 hours forward as tech shares will rise by 15% in the remainder of 2024 from our standpoint with know-how. The basics are set to speed up because the use instances of AI develop materially.”

With that in thoughts, we opened up the TipRanks database to search for two of Ives' shares — well-known tech giants — and see how his views stack up in opposition to the Wall Avenue consensus. Listed here are the main points.

Microsoft (MSFT)

First on our record, Microsoft has been a frontrunner in PCs and working techniques because the 1970s and has develop into one of the crucial iconic model names on the planet. Lately, the Redmond, Washington-based firm has continued its long-standing dedication to advancing know-how, holding a powerful place on the slicing fringe of synthetic intelligence. Microsoft has a long-standing curiosity in AI and was an early supporter of OpenAI, the corporate that introduced us generative AI and GPT Chat in late 2022. The corporate's cumulative funding in OpenAI is round $10 billion.

From a consumer perspective, Microsoft has a number of extremely seen AI initiatives. These embody the mixing of generative AI know-how into the Bing search engine in an effort to make Bing simpler to make use of with an improved interface and search outcomes, aiming to compete extra strongly with Google. Microsoft can also be incorporating AI into updates to its Home windows and Workplace software program packages. Amongst these additions to the flagship software program is Copilot, Microsoft's new AI-powered on-line assistant. Copilot is designed to offer real-time consumer assist knowledgeable by your personal work and content material creation historical past.

Maybe the largest use of synthetic intelligence in Microsoft's product supply may be present in its cloud computing platform, the Azure subscription service. Azure is a set of over 200 cloud-based purposes and instruments, and Microsoft is constructing AI into the platform—clients will be capable to select AI-enhanced variations of Azure purposes. The transfer guarantees to each make Azure an easier-to-use product with better flexibility and make the platform a stronger competitor to Amazon's AWS and Google Cloud.

A take a look at Microsoft's newest monetary report, which coated fiscal 3Q24, reveals that the AI improve to Azure is paying off. Azure is a part of Microsoft's Clever Cloud phase, which generated $26.7 billion in income for the quarter, up 21 p.c year-over-year and up 43 p.c from the quarterly prime line. The corporate's complete income for the fiscal third quarter rose 17% yr over yr to $61.9 billion, beating forecasts by $1.01 billion. Ultimately, Microsoft posted earnings of $2.94 per share, a determine that was 11 cents per share higher than anticipated – and up 20% from the year-ago interval.

Microsoft inventory has proven sturdy efficiency over the previous yr; not stunning given the stable monetary outcomes. Shares have gained 42% over the previous 12 months and are up almost 25% this yr.

For Ives, the important thing level right here is AI's potential to unlock further positive factors as MSFT strikes ahead. He writes: “We expect the inventory shouldn’t be but priced in what we see as the following wave of cloud and AI development coming to the Redmond story, with a powerful aggressive benefit within the cloud, particularly in opposition to Amazon and Google within the cloud bake off Current checks from our companions have been more and more sturdy on Copilot deployments with MSFT clients, and finally we estimate this might add one other ~$25B to Redmond's topline trajectory by 2018 fiscal 25. Right here's the important thing, because the multiplier impression of AI godfather Jensen and Nvidia is simply starting to be felt on the cloud/software program layer because the second spinoff of the AI revolution unfolds on the bottom.”

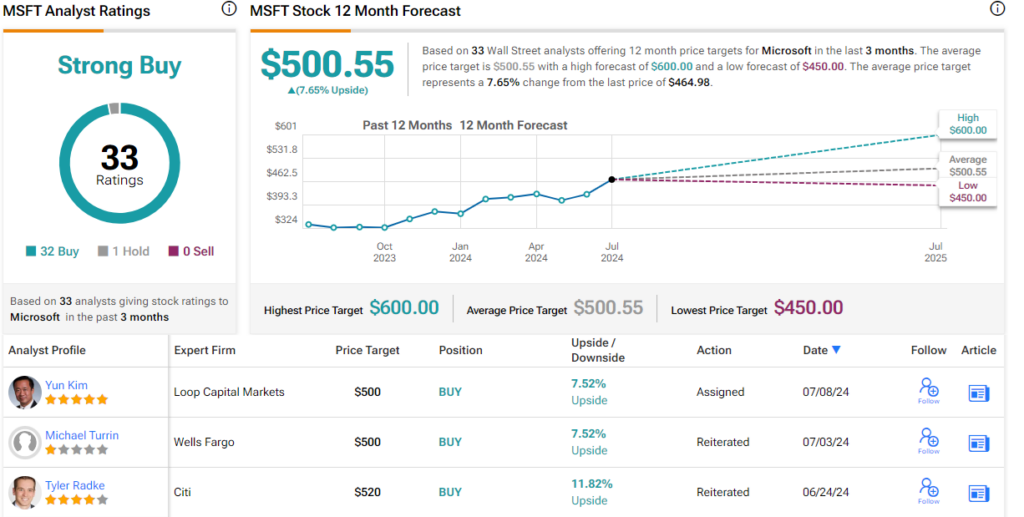

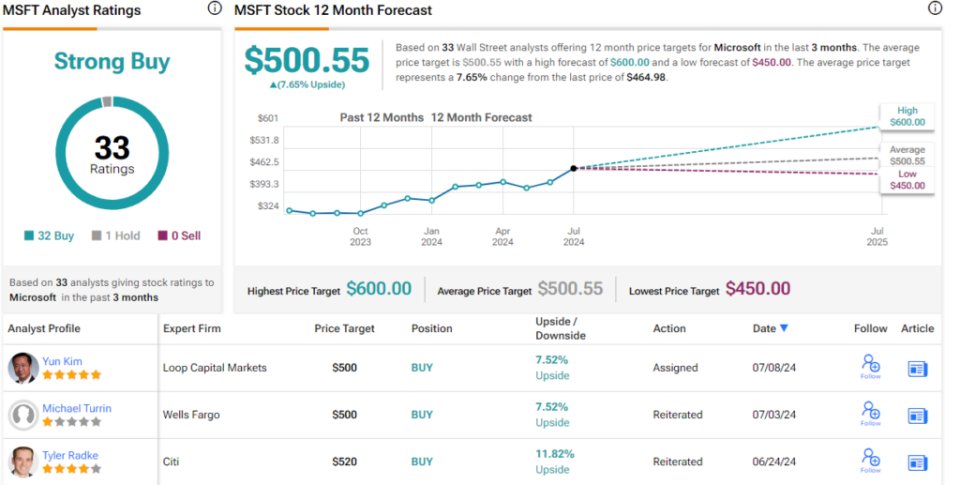

The tech professional continues to offer Microsoft inventory an Outperform (Purchase) ranking, together with a $550 value goal, suggesting a one-year upside potential of 18%. (To trace Ives' observe report, click on right here)

This venerable know-how agency obtained 33 latest analyst critiques, with an uneven break up of 32 Buys to 1 Maintain, giving the inventory a Robust Purchase consensus ranking. The inventory is priced at $464.98, and the common value goal of $500.55 implies it should acquire 7.5% over the following yr. (See MSFT Inventory Forecast)

Salesforce.com (mRCC)

Subsequent is Salesforce, a widely known title within the discipline of buyer relationship administration, or CRM. Salesforce offers a great definition of CRM, describing it as a system for managing an organization's interactions with all clients, present and potential, with the straightforward objective of bettering relationships and rising enterprise.

Salesforce has been within the CRM enterprise since 1999 and has perfected the system. The corporate gives an industry-leading cloud-based software program platform that streamlines CRM actions, together with gross sales calls, advertising emails and customer support interactions. The platform tracks these interactions and creates a unified database of buyer and firm data.

Lately, Salesforce has built-in AI know-how into its CRM software program merchandise, additional enhancing the talents of each builders and customers to customise the platform to suit any enterprise scale or objective. The corporate's AI integration streamlines knowledge retrieval, improves communications, automates repetitive duties, and generates actionable insights via autonomous knowledge evaluation. Salesforce additionally makes use of generative AI for automated inventive functions – producing personalised communications with clients, together with focusing on advertising contacts and figuring out one of the best time to launch them.

Salesforce, in its years of operation, has develop into an important a part of the enterprise universe, offering a mandatory service based mostly on the newest know-how and delivering stable outcomes for its shoppers.

As for Salesforce outcomes, the corporate reported its fiscal 1Q25 monetary launch on the finish of Might and beat the forecast on earnings, excluding income. The corporate's income got here in at $9.13 billion, up almost 11 p.c from a yr earlier, however $20 million lower than anticipated. The underside line was reported at $2.44 by non-GAAP measures, up 44% y/y – and beating estimates by 7 cents per share.

The corporate reported some further numbers that ought to pique investor curiosity, together with $eight.59 billion in subscription and assist income, up 12% year-over-year and a major driver of total income development. Free money circulate rose 43% y/y within the quarter to $6.08 billion. Salesforce ended the quarter with $9.96 billion in money and liquid belongings out there as of April 30 of this yr.

Whereas these outcomes have been stable, Salesforce inventory fell sharply after the discharge — primarily when its Q2 forecast did not impress. The corporate's Q2 income and earnings estimates have been under consensus estimates. Inventory is at present flat for the yr so far.

Dan Ives, in his protection of Salesforce, has an investor's perspective — and is impressed with the corporate's present capabilities and near-term potential. Ives writes of Salesforce: “In our view, CRM is on a path to greater development, margin and FCF trajectory, and that is only a small bump throughout a development transition interval…CRM [remains] considered one of our favourite tech names to personal over the following yr because the AI story begins to take form. We'd be consumers on the weak point… as a result of, seeing the forest via the timber, this can be a shift in movement for a top-tier tech main with an enormous put in base led by the most effective CEOs within the world tech panorama, in our opinion.”

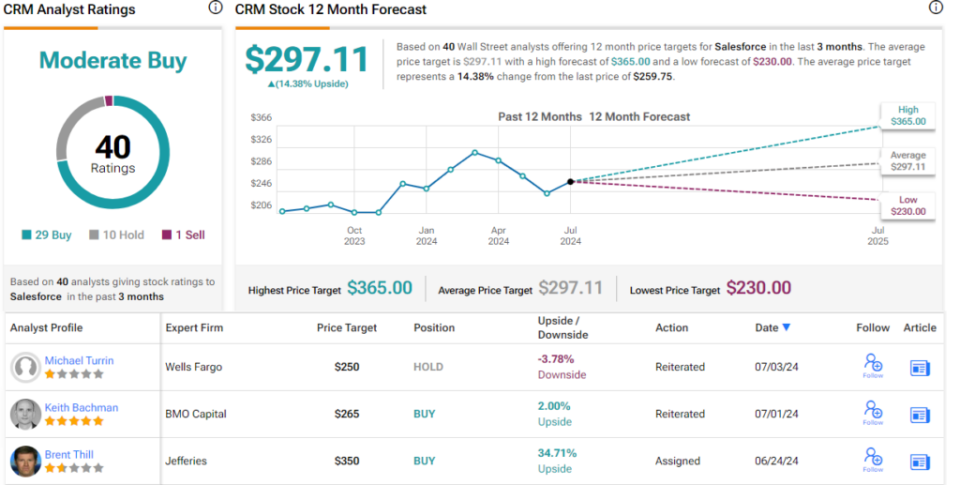

Following these feedback, Ives charges CRM as Outperform (Purchase), with a value goal of $315 suggesting a 21% acquire within the coming months.

There are 40 latest analyst critiques recorded for Salesforce inventory, and break right down to 29 buys, 10 holds and 1 promote, giving the inventory a consensus ranking of Reasonable Purchase. The inventory is priced at $259.81, with a mean value goal of $297.11, indicating a 14% upside potential over a one-year horizon. (See CRM inventory forecast)

To seek out good concepts for buying and selling shares at engaging valuations, go to TipRanks's Greatest Shares to Purchase, a device that aggregates all of TipRanks inventory data.

Disclaimer: The opinions expressed on this article are solely these of the featured analyst. The content material is meant for use for informational functions solely. It is extremely vital to do your personal evaluation earlier than making any funding.