The Exterior Fund Administrator backed by Charlie Muger of Berkshire Hathaway, Li Lu, does nothing about it when he says “the very best funding danger shouldn’t be the volatility of costs, but when it is going to endure a everlasting lack of capital.” Due to this fact, it might be apparent that the debt ought to take into account, when you consider how dangerous any motion is, as a result of an excessive amount of debt can sink an organization. As with many different corporations Caesars Leisure, Inc. (Nasdaq: CZR) Use the debt. However an important query is: how a lot danger is that debt?

Why does the debt deliver dangers?

Debt and different liabilities grow to be dangerous for a corporation after they can not simply adjust to these obligations, both with free money circulate or rising capital at a lovely value. Within the worst case, an organization can go bankrupt in case you can not pay your collectors. Whereas that’s not too widespread, we frequently see that indebted corporations completely dilute shareholders as a result of lenders pressure them to boost capital at an anguished value. After all, debt might be an vital software in corporations, significantly heavy capital corporations. The very first thing to do when contemplating how a lot debt an organization makes use of is to research its money and debt collectively.

Take a look at our final evaluation for Caesars Leisure

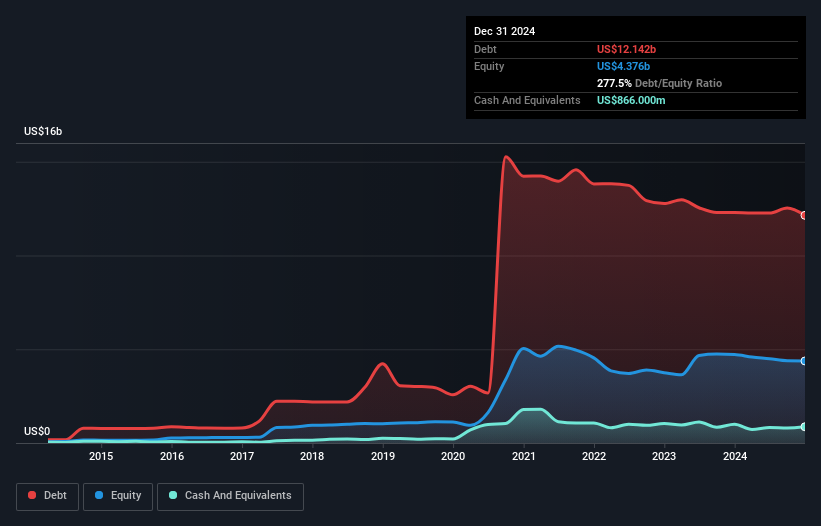

What’s the internet debt of Caesars Leisure?

As you’ll be able to see under, Caesars Leisure had US $ 12.1b of debt, in December 2024, which is nearly the identical because the earlier 12 months. You’ll be able to click on on the desk for extra particulars. Alternatively, it has US $ 866.zero million in money that results in a internet debt of roughly US $ 11.3b.

A have a look at Caesars Leisure liabilities

After I went from the most recent knowledge of the stability sheet, we are able to see that Caesars Leisure had liabilities of US $ 2.27b due in 12 months and liabilities of US $ 25.9b due to that. By compensating this, it had US $ 866.zero million in money and US $ 470.zero million in accounts receivable that had been offered inside 12 months. Due to this fact, your liabilities complete US $ 26.9b greater than the mix of your money and accounts receivable within the quick time period.

This deficit throws a shadow on the corporate of US $ 6.13b, like a colossus that rises over the straightforward mortals. So we might observe your stability carefully, little question. On the finish of the day, Caesars Leisure would most likely want an vital recapitalization if their collectors demanded reimbursement.

We use two principal proportions to tell ourselves about debt ranges in relation to income. The primary is the online debt divided by income earlier than curiosity, taxes, depreciation and amortization (EBITDA), whereas the second is what number of instances its income earlier than curiosity and taxes (EBIT) cowl their curiosity bills (or their curiosity protection, to abbreviate). The benefit of this method is that we bear in mind each absolutely the quantity of debt (with internet debt to Ebitda) and the actual curiosity bills related to that debt (with its curiosity protection ratio).

Though the debt relationship to Ebitda of Caesars Leisure (three.1) means that it makes use of a sure debt, its curiosity protection could be very weak, to zero.96, which suggests a excessive leverage. It appears clear that the price of requested cash is negatively affecting returns to shareholders, in latest instances. One other concern for traders may very well be that Caesars Leisure Ebit fell 11% within the final 12 months. If that’s the means issues proceed to deal with the debt load will likely be like delivering scorching coffees in a pogo stick. The stability is clearly the world to give attention to when it analyzes the debt. However it’s future positive aspects, greater than something, which is able to decide the power of Caesars Leisure to take care of a wholesome stability sooner or later. So, if you wish to see what professionals suppose, you will discover that this free report on analysts’ revenue forecasts is attention-grabbing.

Lastly, a enterprise wants free money circulate to pay the debt; Accounting income merely don’t lower it. So, the logical step is to watch the proportion of that EBIT that coincides with the actual free money circulate. Within the final three years, Caesars Leisure created a free money circulate that amounted to four.three% of its EBIT, a little bit inspiring efficiency. This lazy stage of money conversion undermines its means to manage and pay the debt.

Our opinion

At first look, Caesars Leisure’s curiosity cowl left us tentative in regards to the inventory, and its complete liabilities was no extra engaging than the empty restaurant on the busiest evening of the 12 months. And even its Ebit progress fee doesn’t encourage a lot confidence. Making an allowance for all of the aforementioned elements, plainly Caesars Leisure has an excessive amount of debt. That sort of danger is ok for some, nevertheless it actually doesn’t float in our boat. Given the dangers round using debt by Caesars Leisure, the smart factor is to confirm if consultants have been downloading the actions.

When every little thing is alleged and finished, it’s typically simpler to give attention to corporations that don’t even want debt. Readers can entry a listing of progress actions with internet debt zero 100% freeproper now.

New: Ai inventory inventory and alerts

Our new scan the market scanning daily to find alternatives.

• Dividend powers (three%+ efficiency)

• Small layers undervalued with inner purchases

• Excessive progress and AI know-how corporations

Or construct yours from greater than 50 metrics.

Discover now without cost

Do you might have feedback about this text? Apprehensive about content material? Get in contact With us immediately. Alternatively, ship an e mail to the editorial workforce (AT) simplywallst.com.

This merely wall st article is normal in nature. We offer feedback based mostly on historic and prognostic knowledge of analysts solely utilizing an neutral methodology and our articles don’t intend to be monetary recommendation. It doesn’t represent a advice to purchase or promote any motion, and doesn’t bear in mind its goals or its monetary scenario. Our aim is to offer an extended -term centered evaluation promoted by elementary knowledge. Remember that our evaluation might not bear in mind the final pricing delicate adverts or materials. Merely Wall ST has no place in any talked about motion.